LTD vs LLP vs Sole Trader UK 2026: Which Business Structure is Right for You?

Last Updated on March 20, 2026 by James Hartley

🇬🇧 MEMBER DEAL: ThriveOnz360 Growth members unlock exclusive 1st Formations pricing — SEIS-ready UK Ltd from £12.99 same-day, plus the LTD vs Sole Trader Tax Calculator 2026/27. Free to join.

Choosing the wrong business structure in the UK costs founders thousands per year in unnecessary tax — or exposes them to unlimited personal liability when it could easily be avoided. This guide compares Sole Trader, LLP, and Limited Company (LTD) across every dimension that matters in 2026: true tax liability at £40K, £70K, and £100K profit; the April 2026 dividend tax increase and what to do before it hits; NIC comparison at each level; and a 5-step decision framework for your specific situation. For most founders above £40,000–£50,000 profit, incorporation via 1st Formations (from £12.99, same-day) saves £3,000–£8,000+ per year after admin costs.

🏆 THRIVEONZ360 GUIDE · UK BUSINESS STRUCTURE 2026 · LTD vs LLP vs SOLE TRADER

LTD vs LLP vs Sole Trader UK 2026: Which Business Structure Is Right for You?

The structure that was right at £20,000 profit may be costing you thousands at £80,000. This is not an abstract debate about legal entities — it is a concrete tax calculation with real money at stake. This guide gives you the numbers, the framework, and the steps to act on them.

✅ Tax at £40K / £70K / £100K: all three structures

✅ April 2026 dividend increase — what to do now

✅ NIC comparison: Class 4 vs Class 1 vs Employer

✅ Optimal director salary 2025/26

✅ LLP vs LTD: when each wins

✅ 5-step decision framework

✅ Common mistakes when changing structure

✅ Step-by-step next actions for each path

⚡ KEY NUMBERS 2025/26

CT: 19% (up to £50K) / 25% (above £250K)

Dividend: 8.75% / 33.75% (→ 10.75% / 35.75% from 6 Apr 2026)

Employer NIC: 15% above £5,000 secondary threshold

LTD saves ~£8,000/yr vs sole trader at £100K profit

★ Incorporate via 1st Formations from £12.99

📊 Structure Comparison: At a Glance

19–25%

Corporation Tax on company profits. vs 40% higher-rate income tax as sole trader above £50,270. This 15–21% gap is the fundamental engine of the LTD tax saving.

6 Apr 2026

Dividend tax increases confirmed by Autumn 2025 Budget: basic rate 8.75% → 10.75%; higher rate 33.75% → 35.75%. A director taking £50K dividends will pay ~£1,000 more per year. Act before this date if you have retained profits.

~£8,000

Typical LTD saving vs sole trader at £100,000 profit — after accounting for extra accountant costs (£1,000–2,000/yr). This compounds further if profits are retained rather than fully extracted each year.

£35K–£50K

Typical profit range where incorporation starts to make financial sense. Below: admin costs consume the tax saving. Above: higher-rate income tax makes CT + dividend extraction meaningfully more efficient.

£12.99

Cost to incorporate a UK Ltd via 1st Formations — all-in including the £50 Companies House fee. Same-day processing. SEIS-ready Articles from £52.99. The tax saving in year one at £80K profit is 600× this cost.

⚡ Quick Navigation

- Three Structures At a Glance →

- Sole Trader: Tax, NIC, and When It Works →

- Limited Company: Corporation Tax, Dividends, Director Salary →

- LLP: When It Beats LTD and When It Doesn’t →

- The Numbers: All Three Structures at £40K / £70K / £100K →

- NIC Comparison: The Often-Overlooked Cost Driver →

- 5-Step Decision Framework →

- Common Mistakes When Changing Structure →

- Next Steps for Each Path →

⚠️ Important: This article covers the core numbers and decision framework for UK business structures in 2026. Tax is personal — your specific position depends on your income level, other income sources, family circumstances, pension contributions, and allowable expenses. The calculations shown are illustrative estimates based on simplified assumptions. Always verify your situation with a qualified accountant before changing your structure. 1st Formations incorporates the company; tax planning is your accountant’s role.

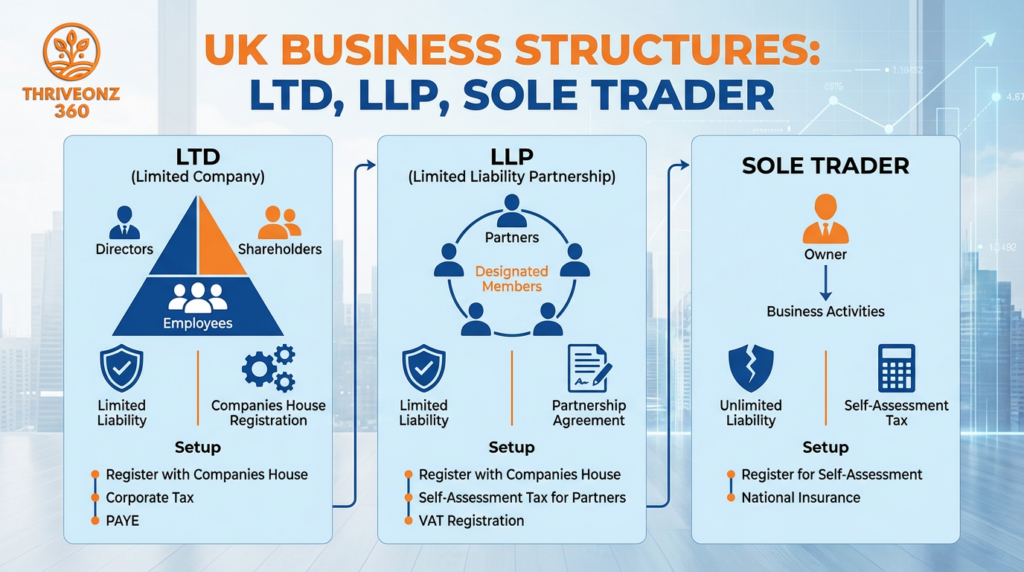

The Three Structures At a Glance

| Factor | Sole Trader | LLP | Limited Company (LTD) ★ |

|---|---|---|---|

| Legal status | No separate entity | Separate legal entity | Separate legal entity |

| Personal liability | Unlimited ❌ | Limited ✅ | Limited ✅ |

| Minimum people | 1 ✅ | 2 minimum ⚠️ | 1 ✅ |

| Tax on profits | Income tax (20–45%) + Class 4 NIC on all profit | Income tax + Class 4 NIC per member (pass-through taxation) | CT 19–25% (company) + income/dividend tax on extraction only |

| Privacy | High — no public filing ✅ | Moderate | Low — accounts, directors, shareholders all public |

| Admin burden | Low ✅ | Medium | Medium–High |

| Accountant cost (typical) | £500–£1,500/yr | £1,200–£3,000/yr | £1,500–£4,000/yr |

| Retain profits at lower tax rate | ❌ All profit taxed immediately | ❌ All profit taxed immediately | ✅ Retained profits taxed at 19–25% CT only |

| Business sale / investment | Complex | Complex — no shares | ✅ Shares easily transferred; BADR may apply |

| Formation cost | Free (HMRC self-reg) | £50+ at Companies House | £12.99 all-in via 1st Formations ✅ |

Sole Trader: The Simplest Starting Point

A sole trader is not a separate legal entity. You and your business are the same person in the eyes of the law. Your business income is your personal income. Your business debts are your personal debts. There is no incorporation, no annual accounts at Companies House, no Corporation Tax return — just one Self Assessment tax return per year.

Income Tax Rates 2025/26

| Band | Income | Rate |

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571–£50,270 | 20% |

| Higher Rate | £50,271–£125,140 | 40% |

| Additional Rate | Above £125,140 | 45% |

Tax Examples — Sole Trader

£50,000 net profit

Income tax on £37,430: 20% = £7,486

Class 4 NIC on £37,430: 6% = £2,246

Total tax: £9,732 → Keep: £40,268 (19.5% effective)

£80,000 net profit

Income tax: £7,540 (basic) + £11,892 (higher) = £19,432

Class 4 NIC: £2,262 + £595 = £2,857

Total tax: £22,289 → Keep: £57,711 (27.9% effective)

✅ Sole Trading Works Well When:

- Turnover is below £30,000–£40,000 — the tax saving from LTD does not offset the £1,000–2,000/yr additional admin and accountant cost

- No meaningful liability risk in your work (design, writing, tutoring, most consulting)

- No clients requiring a limited company structure for procurement or IR35 purposes

- You want minimum admin — one Self Assessment per year covers the entire filing obligation

- Testing a business idea before committing to a structure with ongoing Companies House obligations

⚠️ Sole Trading Creates Problems When:

- Profits consistently clear £40,000–£50,000 — higher-rate income tax (40%) kicks in hard above £50,270; Corporation Tax (19%) on the same profit looks very different

- Your work carries personal liability risk: construction, professional advice, healthcare, product manufacturing, property — unlimited liability is a serious exposure

- Larger companies or public sector bodies will not engage without a limited company for procurement compliance or IR35 reasons

- You want to retain profits in the business rather than extracting — all sole trader profit is taxed immediately at your marginal rate regardless of whether you draw it

- You plan to sell the business or bring in a business partner or investor

Limited Company (LTD): The Tax and Liability Vehicle

A private limited company is a separate legal entity. It owns its own assets, incurs its own liabilities, and has its own tax obligations. Shareholders are protected from company debts beyond the nominal value of their shares — typically £1. The director and shareholder are usually the same person in small owner-managed companies.

The core LTD tax mechanism: Company profits are taxed at Corporation Tax (19–25%) rather than income tax (20–45%). You extract money as a combination of salary (small, to use the personal allowance and maintain NIC record) plus dividends (which carry no NIC and are taxed at dividend rates, not income tax rates). The gap between 19% CT and 40% higher-rate income tax is the engine of the LTD saving.

Corporation Tax Rates 2025/26 (Unchanged for FY2026)

| Profit Level | CT Rate |

| Up to £50,000 | 19% (Small Profits Rate) |

| £50,001–£250,000 | 19–25% via Marginal Relief effective marginal rate 26.5% in band |

| Over £250,000 | 25% (Main Rate) |

⚠️ Dividend Tax Rates — Current vs 6 April 2026

| Band | Now (2025/26) | From 6 Apr 2026 |

| Dividend Allowance | £500 at 0% | £500 at 0% |

| Basic Rate | 8.75% | 10.75% ↑ |

| Higher Rate | 33.75% | 35.75% ↑ |

| Additional Rate | 39.35% | 39.35% |

Optimal Director Salary 2025/26 — Why Salary + Dividends, Not Salary Alone

Dividends are paid from post-Corporation-Tax profits and carry no National Insurance. Salary is subject to employee NIC (8%) and — for sole directors without Employment Allowance — employer NIC (15% above the £5,000 secondary threshold from April 2025). The correct extraction strategy is a carefully calibrated salary plus the remainder as dividends.

£12,570/year salary — most common

Uses full personal allowance. No income tax on salary. Employer NIC: 15% on £7,570 (£12,570 minus £5,000 threshold) = £1,135. CT saving from salary deduction: £7,570 × 19% = £1,438 — more than offsets employer NIC at the small profits rate. Net benefit: £303.

£9,100/year — avoids employer NIC

Below the £5,000 secondary threshold. No employer NIC cost. But you lose the CT saving on salary from £9,100 to £12,570. The optimal salary point shifts if CT rate is 25% (main rate). Always model the specific numbers with your accountant.

Limited Company Administration — The Full Obligation List

Corporation Tax return (CT600) — filed with HMRC within 12 months of accounting period end; tax paid 9 months and 1 day after period end

Annual accounts at Companies House — due 9 months after year end from second year (21 months for first accounts). These are public record. Small companies can file micro-entity accounts disclosing minimal financial detail.

Confirmation Statement (£34/yr) — annual declaration confirming director/shareholder details. The most-missed compliance obligation for new Ltd directors.

Director’s Self Assessment — required even with only salary and dividend income from your own company. You cannot use PAYE-only filing.

PAYE/RTI submissions — if paying a salary, you must register as an employer and submit a Full Payment Submission to HMRC on or before every payment date. See: UK PAYE RTI Guide 2026 →

Dividend paperwork — each dividend payment requires a board minute and dividend voucher. Missing these risks HMRC reclassifying dividends as disguised salary and charging employer NIC + penalties.

ThriveOnz360 — Growth Plan

LTD vs Sole Trader Tax Calculator 2026/27 — Model Your Specific Numbers

Growth members unlock: LTD vs Sole Trader Tax Calculator (model take-home at your profit level including April 2026 dividend tax increases) + UK Business Structure Comparison Guide (£30K–£150K) + Limited Company Setup Checklist (38 steps). Free forever.

LLP: The Professional Partnership Structure

How an LLP Is Taxed

An LLP does not pay Corporation Tax. Each member pays income tax on their allocated profit share through Self Assessment — exactly like a sole trader. The same income tax rates and Class 4 NIC that apply to a sole trader apply to an LLP member on their profit share.

Key NIC advantage: No employer NIC on profit distributions to LLP members. Members are self-employed, not employees. At 15% (from April 2025), this is a significant saving versus paying equivalent salaries to employees.

LLP member with £60,000 profit share:

Income tax: £11,432

Class 4 NIC: £2,457

Total: £13,889 → Keep: £46,111

LLP Legal Requirements

- Minimum two members — no maximum; can be individuals or corporate entities

- UK registered office address (same requirement as Ltd)

- LLP Agreement (strongly recommended — without it, default LLP Act 2000 terms apply, which may not reflect your intentions on profit sharing, decision-making, or exit)

- Annual accounts at Companies House (similar to LTD — public record)

- Partnership Self Assessment return (SA800) plus individual SA per member

| Criterion | LLP Advantage | LTD Advantage |

|---|---|---|

| Employer NIC on profit distributions | ✅ None — members are self-employed | 15% employer NIC on salary component |

| High earner (£100K+ per member) | 40% income tax on all profit above £50,270 | ✅ 19–25% CT on retained profits |

| Retaining profits to reinvest | All profits taxed immediately at income tax rate regardless of extraction | ✅ Retained profits compound at 19–25% CT only |

| Business sale or investment | Complex — no shares to sell; goodwill disposal only | ✅ Shares easily transferred; Business Asset Disposal Relief may apply (10% CGT) |

| Moderate profit per member (<£100K) | ✅ Often more efficient — no employer NIC on profit shares | CT + dividend route competitive but not clearly superior |

| Member departs — single-member risk | ❌ Reverts to unlimited-liability general partnership if not resolved in 6 months | ✅ No issue — Ltd continues with one director/shareholder |

✅ Choose LLP When:

- Two or more genuine partners with shared management responsibility

- Professional services sector where LLP is the norm (solicitors, accountants, architects, GPs)

- Profit per member is moderate (<£100,000) — CT + dividend route not clearly superior

- Your professional body requires or strongly prefers a partnership structure

- You value self-employed tax status — no employer NIC on profit distributions

- You do not intend to retain profits or sell the business

❌ LLP Less Appropriate When:

- Only two partners — single-member liability risk if one leaves

- You want to retain and reinvest profits at a lower tax rate

- Planning to sell the business — LTD shares are far simpler to transfer

- Want to bring in external investors (equity investment requires shares)

- Profit per member exceeds £100,000 — CT + dividend route typically wins

- You are the sole founder with no genuine partner (LLP requires 2 minimum)

The Numbers: All Three Structures at £40K, £70K, and £100K Profit

Assumes single director–shareholder, no other income, £12,570 salary, remainder as dividends (LTD), or full profit extraction (Sole Trader/LLP). 2025/26 rates throughout. These are illustrative estimates — your position depends on allowable expenses, pension contributions, and all income sources.

£40,000 Profit — Sole Trader Ahead

Sole Trader / LLP member

Income tax: ~£7,466

Class 4 NIC: ~£1,664

Total: ~£9,130 → Keep: ~£30,870

Limited Company

CT + employer NIC + dividend tax: ~£10,200

Keep: ~£29,800 (worse by ~£1,070)

£70,000 Profit — Near-Identical

Sole Trader / LLP member

Income tax: ~£16,432

Class 4 NIC: ~£2,647

Total: ~£19,079 → Keep: ~£50,921

Limited Company

CT + employer NIC + dividend tax: ~£17,500

Keep: ~£52,500 (better by ~£1,579)

£100,000 Profit — LTD Clearly Wins

Sole Trader / LLP member

Income tax: ~£29,460

Class 4 NIC: ~£3,557

Total: ~£33,017 → Keep: ~£66,983

Limited Company

CT + employer NIC + dividend tax: ~£25,000

Keep: ~£75,000 (better by ~£8,017)

⚠️ April 2026 Dividend Tax Increase — Genuine Planning Window Before 6 April 2026

A director taking £50,000 in dividends will pay approximately £1,000 more per year from 6 April 2026 (basic rate 8.75% → 10.75%). Higher-rate dividend taxpayers face an increase of £1,000 per £50,000 of higher-rate dividends. If you have retained profits in your company and planned to take dividends in the 2026/27 tax year, taking them before 6 April 2026 captures the lower 2025/26 rates. Dividends must be declared AND paid before 6 April 2026 to qualify for current rates.

This is a genuine timing opportunity for directors with retained profits. Discuss with your accountant as soon as possible — processing and paperwork take time.

NIC Comparison — The Often-Overlooked Cost Driver

| NIC Type | Sole Trader | LLP Member | LTD Director (salary + dividends) |

|---|---|---|---|

| On profit/salary | Class 4: 6% on £12,571–£50,270; 2% above | Class 4: 6% on £12,571–£50,270; 2% above (same as ST) | Class 1: 8% on salary £12,571–£50,270 (salary only — much smaller base) |

| Employer NIC | None ✅ | None on profit shares ✅ | 15% on salary above £5,000 secondary threshold (from Apr 2025) |

| On dividends | N/A | N/A | None — dividends carry zero NIC ✅ |

| Employment Allowance (£10,500/yr from Apr 2025) | Not available | Not available | Not available for single-director companies. Available if you have other employees — can offset up to £10,500 employer NIC. |

Why NIC Changes the Picture at High Profit Levels

A sole trader with £80,000 profit pays Class 4 NIC on approximately £67,430 (the full amount above the threshold). An LTD director extracting the same £80,000 pays employer NIC only on the salary component (~£12,570), with all dividends carrying zero NIC. At this level, the NIC difference alone is thousands per year — one of the primary drivers of the LTD advantage above £70K profit. From April 2025, employer NIC rose from 13.8% to 15% and the secondary threshold fell to £5,000, increasing the salary cost for Ltd companies. Review your salary point with your accountant given the updated rates.

Tax Comparison Summary — All Three Structures at Three Profit Levels

| Structure | £40,000 Profit | £70,000 Profit | £100,000 Profit |

|---|---|---|---|

| Sole Trader | Tax: ~£9,130 Keep: ~£30,870 ✅ Best at this level |

Tax: ~£19,079 Keep: ~£50,921 Borderline vs LTD |

Tax: ~£33,017 Keep: ~£66,983 ❌ ~£8K behind LTD |

| LLP (per member) | Tax: ~£9,130 Keep: ~£30,870 Same as sole trader |

Tax: ~£19,079 Keep: ~£50,921 Same as sole trader |

Tax: ~£33,017 Keep: ~£66,983 Same per-member rate, no employer NIC advantage |

| Limited Company | Tax: ~£10,200 Keep: ~£29,800 ❌ Worse before admin costs |

Tax: ~£17,500 Keep: ~£52,500 Marginally ahead; model carefully |

Tax: ~£25,000 Keep: ~£75,000 ✅ ~£8,000 ahead — clear winner |

5-Step Decision Framework: Which Structure Is Right for You?

Step 1 — Do You Need Liability Protection?

If your business could create debt or legal claims against you personally — construction, professional advice, healthcare, product manufacturing, property, financial advice — you need limited liability. Choose LTD or LLP. If your business has no meaningful liability risk (tutoring, copywriting, low-risk consulting where you deliver services and advice, not products carrying product liability or regulated outputs), liability may not be the primary driver of the decision. But be honest about your risk profile — liability claims are rare until they happen, at which point the protection is invaluable.

Step 2 — Are There Two or More Genuine Partners?

If yes and you are in professional services → consider LLP alongside LTD and compare the two options at your expected profit-per-member level. If yes but you want to retain profits in the business or plan to sell → LTD is usually better. If no (sole founder) → the decision is between sole trader and LTD. LLP requires a minimum of two members — it is not available to a sole founder regardless of other factors.

Step 3 — What Are Your Current and Expected Annual Profits?

| Annual Profit | Typical Recommendation | Reasoning |

| Under £20,000 | Sole trader | Tax saving too small to justify £1,000–2,000/yr extra admin cost + accountant premium |

| £20,000–£35,000 | Sole trader (review at £35K) | Liability risk or client requirements may override the tax numbers at this level |

| £35,000–£50,000 | Borderline — model with accountant | May break even or save slightly; liability and professional image often decide it |

| £50,000–£100,000 | LTD typically beneficial | Higher-rate income tax vs CT + dividend extraction materially more efficient above £50,270 |

| Over £100,000 | LTD strongly advantageous | ~£8,000/yr saving; pension contributions and profit retention amplify further |

Step 4 — Do Your Clients Care About Your Structure?

Large corporates, public sector bodies, and regulated businesses often prefer to contract with limited companies for procurement compliance and IR35 assessment purposes. If a significant client or contract requires a limited company, that may be the deciding factor regardless of where you sit in the tax comparison above. This is particularly common in IT, consulting, financial services, and government work.

Step 5 — Are You Caught by IR35?

IR35 is the off-payroll working legislation that catches contractors who operate through personal service companies but are functionally employees of their clients. If you are inside IR35, the tax advantage of the LTD structure largely disappears — income is treated as employment income and taxed accordingly at PAYE rates. For medium/large-client engagements, the client determines IR35 status. For small-client work, the contractor self-assesses. See IR35 and EOR UK Contractor Compliance 2026 → If IR35 applies to your main work, your accountant should assess your status before you incorporate.

Stay Sole Trader If:

- Profit consistently below £35,000

- No meaningful personal liability risk

- No clients requiring limited company

- Minimum admin is the priority

- Testing a business idea

Consider LLP If:

- Two or more genuine partners in professional services

- Want liability protection + self-employed tax treatment

- Profit per partner under £100,000

- Professional body requires partnership

- Not planning to retain profits or sell

Incorporate LTD If:

- Profit consistently exceeds £40,000–£50,000

- Personal liability risk from your work

- Large clients prefer limited company

- Want to retain and reinvest profits

- Plan to sell the business or bring investors

- IR35 does not apply to your situation

Common Mistakes When Choosing or Changing Structure

Incorporating Too Early

Before profits justify it. Additional accountant cost (£1,000–2,000/yr more), bank charges, payroll administration, dividend paperwork, and annual accounts overhead outweighs any tax saving below £35,000–£40,000 net profit. The tax calculation looks attractive in isolation — the full admin cost picture changes it.

Not Taking a Proper Salary

Directors who pay themselves only dividends miss qualifying years for the State Pension and may attract HMRC scrutiny about whether dividends are genuine distributions. Most accountants recommend a minimum salary at or above the Lower Earnings Limit (£6,396 for 2025/26) to maintain a NIC record, with the optimal level typically around £9,100–£12,570 depending on your specific situation.

Treating the Company Account as a Personal Wallet

Paying personal expenses from the company account creates Director’s Loan Account issues (must be repaid within 9 months or triggers a S455 tax charge at 33.75%) or benefit-in-kind exposures. Common HMRC targets: personal mobile phones, personal car costs, home broadband beyond genuine business proportion. The company account is the company’s money — not yours until formally extracted as salary or dividend.

No Shareholders’ Agreement or LLP Agreement

In an LLP or multi-shareholder LTD, a formal agreement governs what happens if a partner or shareholder leaves, dies, or wants to sell. Without one, disputes default to statutory rules that rarely reflect the founders’ actual intentions. Have the agreement drafted when the structure is created — retrofitting one after a dispute begins costs far more than prevention.

Missing Companies House Filing Deadlines

Accounts must be filed within 9 months of year-end (21 months from incorporation for first accounts). Late filing triggers automatic penalties from £150, escalating steeply to £1,500 for delays beyond 6 months. Companies House penalties are applied automatically with very limited appeal grounds. Set calendar reminders from day one — these deadlines have no grace period.

Not Reviewing the Structure as the Business Grows

The optimal extraction strategy at £50,000 profit is not the same as at £150,000. An annual review with your accountant — covering salary level, dividend timing, pension contributions, VAT scheme, the April 2026 dividend changes, and Employment Allowance eligibility — typically pays for itself multiple times over. The tax environment changes annually; static strategies deteriorate.

Next Steps — Making It Official

Staying as Sole Trader

- ☐ Register with HMRC Self Assessment (deadline: 5 October following the first tax year you started trading)

- ☐ Register for VAT if turnover has exceeded or will exceed £90,000

- ☐ Set up MTD-compliant accounting software (Xero Simple from £7/month — ITSA-specific plan)

- ☐ Engage accountant for Self Assessment — typically pays for itself through correctly claimed expenses

- ☐ Review position at £35,000 profit — that is when to run the incorporation model

Incorporating a Limited Company

- ☐ Check company name availability at Companies House

- ☐ Decide share structure (100 ordinary shares typical; consider spouse as shareholder for dividend income splitting — seek advice on settlements legislation)

- ☐ Incorporate via 1st Formations from £12.99 — same-day, registered office included, SEIS-ready Articles from £52.99

- ☐ Open business bank account (Starling, Monzo Business, Tide — free at entry level)

- ☐ Register as employer with HMRC before paying the first salary

- ☐ Set up accounting software and invite accountant with advisor access

Transitioning from Sole Trader to LTD

- ☐ Time the transition to tax year end (5 April) or accounting period end — mid-year changes add complexity to both sole trader cessation and first LTD period

- ☐ Accountant closes sole trader books + files the cessation period Self Assessment return

- ☐ Notify existing clients — the company is a new legal entity; existing contracts may need novation to transfer to the new company

- ☐ Value assets transferred from yourself to the company — capital gains considerations apply to appreciated assets (IP, equipment purchased at lower cost)

- ☐ Update all business stationery, invoices, and website with company name, registered number, and registered office address — legally required on all company communications

Frequently Asked Questions

Q: At what profit level should I incorporate?

The widely cited range is £35,000–£50,000 net profit (after business expenses). Below £35,000, additional accountant cost and administration typically consume the tax saving. Above £50,000, the saving on higher-rate income tax versus Corporation Tax + dividend extraction becomes meaningful. The April 2026 dividend tax increase narrows the margin slightly for basic-rate taxpayers but increases it for higher-rate. Model the specific numbers with your accountant — this is not a one-size-fits-all calculation.

Q: What are SEIS-ready Articles and do I need them?

SEIS (Seed Enterprise Investment Scheme) gives investors 50% income tax relief on investments up to £200,000 in qualifying UK startups. To qualify, a company’s Articles must not permit preference shares — which Companies House Model Articles allow by default. If you plan to raise SEIS investment, 1st Formations’ Smart Package (£52.99) includes SEIS-optimised Articles configured from day one, saving £1,500–4,000 in solicitor restructuring costs later. If you have no investment plans, Model Articles are fine. See SEIS and EIS Guide 2026 →

Q: What is the difference between a director and a shareholder?

A director manages the company day-to-day and has legal duties under the Companies Act 2006. A shareholder owns shares in the company and receives dividends. In a one-person company you are typically both. In partnerships, a spouse or business partner can be a shareholder without being a director — receiving dividends from the company without management responsibilities. Share structure needs careful design from day one; changing it later can trigger stamp duty and capital gains tax considerations.

Q: Can I be both director and employee of my limited company?

Yes. A company director is an officer of the company and can also be employed under a contract of service. Most small company owner-directors pay themselves a salary via PAYE and take dividends on top of that salary. This is the standard structure and is fully recognised by HMRC — the key is ensuring the dividend paperwork (board minutes and dividend vouchers) is correctly maintained to withstand scrutiny.

Q: Do I need a registered office address for a limited company?

Every limited company and LLP must have a UK registered office address — it appears on the public Companies House register and receives all statutory mail from Companies House and HMRC. Many owner-directors use their home address, which is legal but makes it permanently and publicly visible. 1st Formations provides a central London registered office address from £39.99/year, keeping your home address off the public record. See: Companies House vs 1st Formations vs Rapid Formations UK 2026 →

Q: Do I need a business bank account for my limited company?

Yes, in practice. A limited company is a separate legal entity and its finances must be kept completely separate from your personal finances. Mixing funds creates accounting problems, tax complications, and HMRC scrutiny. Starling Business, Monzo Business, and Tide open accounts quickly (often same week) with no monthly fee at entry level. See: Best UK Business Bank Accounts 2026 →

Q: What happens to my sole trader debts when I incorporate?

Personal debts incurred as a sole trader remain your personal liability — they do not transfer to the new limited company. Going forward, the limited company incurs its own debts which are the company’s liability, not yours personally (unless you have given personal guarantees — common for bank loans and commercial leases). The forward-looking liability protection is one of the key financial benefits of incorporation.

Q: LLP vs LTD — which is better for a two-person professional firm?

For most two-person firms: LTD, unless your professional body requires partnership structure or the two-member LLP risk is manageable. The specific advantage of LLP — no employer NIC on profit distributions — is real but not decisive at moderate profit levels. The critical LLPrisk — reverting to unlimited-liability general partnership if one member leaves — is a practical concern that most two-person firms prefer to avoid by choosing LTD. Model both structures at your specific profit level with your accountant before deciding.

ThriveOnz360 — 1st Formations + Structure + Accounting Tools

Incorporate and Set Up Accounting in One Day — From £12.99

Growth members unlock: LTD vs Sole Trader Tax Calculator 2026/27 (model your specific numbers including April 2026 dividend changes) + UK Business Structure Comparison Guide (£30K–£150K profit levels) + Limited Company Setup Checklist (38 steps) + exclusive 1st Formations pricing. Free forever — no credit card.

Related Articles

UK Formation and Structure

- Companies House vs 1st Formations vs Rapid Formations UK 2026 →

- 1st Formations Review UK 2026: Full Honest Assessment →

- How to Register a Company in the UK 2026: Step-by-Step Guide →

- UK Company Formation Checklist: 10 Steps Before You Launch →

- UK vs Singapore: Where to Incorporate 2026 →

UK Tax and Compliance

Accounting and Banking

- Best Accounting Software UK 2026: Top 10 for SMEs →

- Best UK Business Bank Accounts 2026 →

- Best Expense Management Software 2026: Dext vs Expensify vs Hubdoc →

Investment and Growth

Disclosure: ThriveOnz360 is a partner of 1st Formations UK. We earn a commission when readers incorporate via our affiliate link (1st-formations-limited.sjv.io/3JGznn) at no additional cost to you. Last updated: February 2026. Tax figures reflect 2025/26 rates as confirmed by HMRC. Dividend tax changes (basic rate 10.75%, higher rate 35.75%) take effect 6 April 2026 as confirmed by the Autumn 2025 Budget. Employer NIC rate 15% and secondary threshold £5,000 took effect 6 April 2025. Corporation Tax rates (19% small profits rate up to £50,000; 25% main rate over £250,000) confirmed unchanged for the financial year beginning 1 April 2026. Class 4 NIC: 6% on profits £12,570–£50,270; 2% above. VAT registration threshold: £90,000 (from April 2024). 1st Formations pricing: from £12.99 — verify current pricing at 1stformations.co.uk. All tax calculations in this article are illustrative estimates based on simplified assumptions — actual tax position varies based on allowable expenses, pension contributions, additional income sources, and individual circumstances. The LTD tax calculations assume full extraction of profits as salary plus dividends; where profits are retained in the company, the comparison changes materially in LTD’s favour. This article provides general information only and does not constitute tax, legal, or financial advice. Always consult a qualified accountant or tax adviser before changing your business structure.

Former City of London fintech advisor and SME growth strategist with 12 years building lean tech stacks for founders across the UK and Southeast Asia. James has guided 500+ SMEs through software decisions that cut costs and unlock growth — and believes every founder deserves a trusted, independent voice on their side. Every review published on ThriveOnz360 follows the platform’s Editorial Standards — tools are independently assessed against UK-specific criteria including HMRC compliance, GBP pricing, FCA registration, and IR35 implications.