💷 The Structure That Made Sense at £20,000 May Be Costing You Thousands at £80,000

You Started as a Sole Trader. Something Has Shifted.

- Your income is growing — £50,000, £80,000, £100,000+

- A client asked whether you trade as a limited company

- You heard directors pay themselves in dividends and wonder if you’re leaving money behind

- A solicitor warned that unlimited personal liability is a real risk for what you do

- The question is whether your current structure still makes sense — or whether it’s quietly costing you

✅ What This Guide Gives You

Specific tax numbers: sole trader vs LTD vs LLP at £40K / £70K / £100K profit

The April 2026 dividend tax increase — what changes and what to do before then

NIC comparison: Class 4 vs Class 1 vs employer NIC at each income level

When LLP beats LTD — and when it doesn’t

A 5-step decision framework that works at your specific profit level

📋 2025/26 Key Numbers — Structures at a Glance

19–25%

Corporation Tax rate on company profits — vs 40% higher-rate income tax as sole trader above £50,270

6 April 2026

Dividend tax rises confirmed: basic rate 8.75% → 10.75%; higher rate 33.75% → 35.75%

~£8,000/yr

Typical LTD saving vs sole trader at £100K profit — after accounting for extra admin costs

£35K–£50K

Typical profit range where incorporation starts to make financial sense — model with your accountant

⚡ Quick Actions

- 1st Formations — Incorporate Your Limited Company from £12.99, Same-Day → — 1M+ UK companies incorporated, digital documents, registered office included

- Xero — 30-Day Free Trial + Exclusive ThriveOnz360 Member Rates → — MTD-compliant for all structures: sole trader, LLP, and limited company

- UK Registered Office Address Services 2026 → — every limited company needs one; from £39/year with 1st Formations

- 1st Formations vs Rapid Formations 2026 → — full formation agent comparison

- Best Business Bank Account UK 2026 → — open the right account once incorporated

- Making Tax Digital for Small Business 2026 → — MTD obligations for your chosen structure

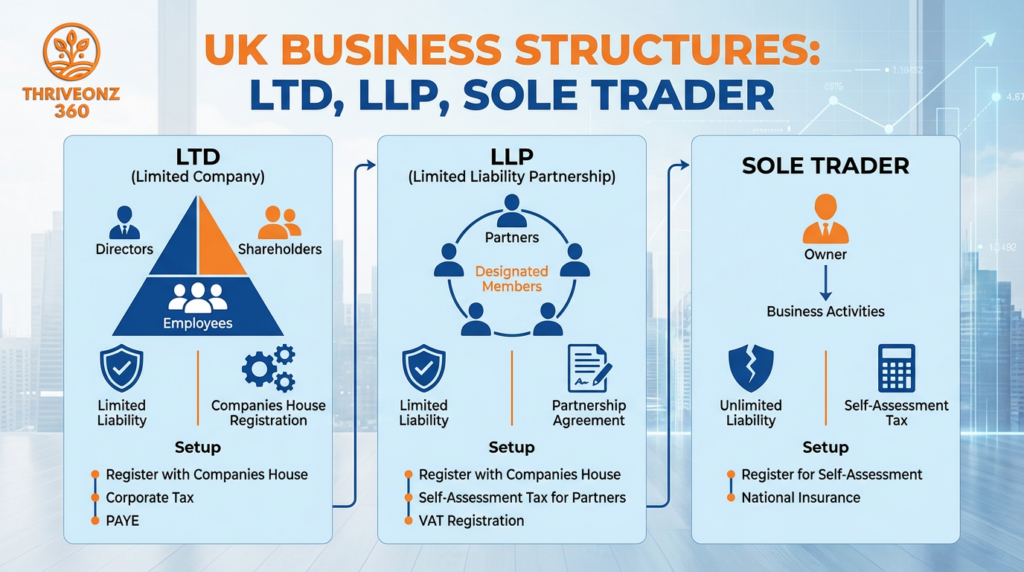

The Three Structures at a Glance

| Factor | Sole Trader | LLP | Limited Company (LTD) |

|---|---|---|---|

| Legal status | No separate entity | Separate legal entity | Separate legal entity |

| Personal liability | Unlimited | Limited | Limited |

| Minimum people | 1 | 2 | 1 |

| Tax on profits | Income tax + Class 4 NIC | Income tax + Class 4 NIC (per member) | Corporation Tax (company) + income/dividend tax (director) |

| Privacy | High — no public filing | Moderate | Low — accounts, directors, shareholders all public |

| Admin burden | Low | Medium | Medium–High |

| Accountant cost (typical) | £500–£1,500/yr | £1,200–£3,000/yr | £1,500–£4,000/yr |

Sole Trader: The Simplest Starting Point

A sole trader is not a separate legal entity — you and your business are the same person in the eyes of the law. Your business income is your personal income. Your business debts are your personal debts.

Income Tax Rates 2025/26

| Band | Income | Rate |

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571–£50,270 | 20% |

| Higher Rate | £50,271–£125,140 | 40% |

| Additional Rate | Above £125,140 | 45% |

Class 4 NIC on top: 6% on profits £12,570–£50,270. 2% on profits above £50,270. Class 2 NIC no longer compulsory — profits above £6,845 auto-credited with State Pension qualifying year.

Tax Examples — Sole Trader

£50,000 net profit

Income tax: 20% on £37,430 = £7,486

Class 4 NIC: 6% on £37,430 = £2,246

Total: £9,732 → Keep: £40,268 (effective rate 19.5%)

£80,000 net profit

Income tax: £7,540 + £11,892 = £19,432

Class 4 NIC: £2,262 + £595 = £2,857

Total: £22,289 → Keep: £57,711 (effective rate 27.9%)

✅ Sole Trading Works Well When:

- Turnover below £30,000–£40,000 — tax saving doesn’t offset LTD admin cost

- No meaningful liability risk (design, consulting, writing, tutoring)

- No clients requiring a company structure

- You want minimum admin — one Self Assessment per year is the entire filing obligation

- Testing a business idea before committing to a structure

⚠️ Sole Trading Creates Problems When:

- Profits consistently clear £40,000–£50,000 — higher-rate income tax bites hard

- You carry personal liability for work that could go wrong (construction, professional advice, manufacturing)

- Larger companies or public sector will not engage without a limited company

- You want to separate personal and business finances for mortgage applications or business sale

Limited Company (LTD): The Tax and Liability Vehicle

A private limited company is a separate legal entity. Shareholders are protected from company debts up to their share capital — typically £1. In most small companies, the director and shareholder are the same person.

Step 1: Corporation Tax on Company Profits

| Profit Level | CT Rate |

| Up to £50,000 | 19% (Small Profits Rate) |

| £50,001–£250,000 | 19–25% via Marginal Relief (effective marginal rate 26.5% in band) |

| Over £250,000 | 25% (Main Rate) |

Rates confirmed unchanged for financial year beginning 1 April 2026. Associated companies warning: If you control multiple companies, the £50,000 and £250,000 thresholds are divided between them.

Step 2: Dividend Tax Rates — Current vs April 2026

| Band | 2025/26 | From 6 Apr 2026 |

| Dividend Allowance | £500 at 0% | £500 at 0% |

| Basic Rate | 8.75% | 10.75% ↑ |

| Higher Rate | 33.75% | 35.75% ↑ |

| Additional Rate | 39.35% | 39.35% |

Confirmed by Autumn 2025 Budget. Any dividends paid on or after 6 April 2026 taxed at new rates. See planning note below.

Optimal Director Salary (2025/26) — Why Salary + Dividends, Not Salary Alone

Dividends are paid from post-Corporation-Tax profits and carry no National Insurance. Salary is subject to employee NIC (8%) and — for sole directors without the Employment Allowance — employer NIC (15% above £5,000 secondary threshold from April 2025).

£12,570/year salary — most common

Uses full personal allowance. No income tax on salary. Employer NIC of 15% on £7,570 (£12,570 minus £5,000 threshold) = £1,135.50. Corporation Tax saving from salary deduction: £7,570 × 19% = £1,438 — more than offsets employer NIC at the small profits rate.

£9,100/year — avoids employer NIC

Below £5,000 secondary threshold. No employer NIC cost. But you lose the Corporation Tax saving on the additional salary from £9,100 to £12,570. Optimal point depends on your CT rate. Always model with your accountant.

ThriveOnz 360 — Growth Plan

Model Your Take-Home: LTD vs Sole Trader Tax Calculator 2026/27

Growth members: LTD vs Sole Trader Tax Calculator (model your take-home at your specific profit level including April 2026 dividend tax increases and updated employer NIC) + UK Business Structure Comparison Guide (£30K–£150K profit levels) + Limited Company Setup Checklist (38 steps). Free to join.

The Numbers: LTD vs Sole Trader at Three Income Levels

Assumes single director–shareholder, no other income, £12,570 salary, remainder as dividends. 2025/26 rates throughout. These are illustrative estimates — your position depends on allowable expenses, pension contributions, and income sources.

£50,000 Profit — Sole Trader Ahead

Sole Trader

Tax: £9,732 → Keep: £40,268

Limited Company

CT + employer NIC + dividend tax = £10,560 → Keep: £39,440

Verdict: Sole trader keeps £828 more before admin costs. Below this level, the additional accountant cost (£1,000–2,000/yr) clearly outweighs incorporation.

£80,000 Profit — Near-Identical Take-Home

Sole Trader

Tax: £22,289 → Keep: £57,711

Limited Company

CT + employer NIC + dividend tax = £22,386 → Keep: £57,614

Verdict: Almost identical (~£100 difference). Tax composition differs dramatically but total is the same. Liability protection and client requirements may be the deciding factor here.

£100,000 Profit — LTD Meaningfully Ahead

Sole Trader

Tax: ~£34,050 → Keep: ~£65,950

Limited Company

Tax: ~£26,000 → Keep: ~£74,000

Verdict: LTD saves ~£8,000/year after typical additional accounting costs. This compounds further if profits are retained in the company rather than all extracted.

⚠️ April 2026 Dividend Tax Increase — Planning Opportunity

A director taking £50,000 in dividends will pay approximately £1,000 more per year from 6 April 2026. If you have retained profits and planned to take dividends in the 2026/27 tax year, taking them before 6 April 2026 captures the lower 2025/26 rates. Dividends declared and paid before 6 April 2026 are taxed at current rates. Discuss with your accountant — this is a genuine timing opportunity for those in a position to act on it.

Limited Company Administration — The Reality

Accountant cost difference: LTD £1,500–£3,500/yr vs sole trader £500–£1,500/yr. The £1,000–£2,000 additional annual cost must be factored into any “incorporation saves money” calculation.

LLP: The Professional Partnership Structure

How an LLP Is Taxed

An LLP does not pay Corporation Tax. Each member pays income tax on their allocated profit share — exactly like a sole trader — reported through Self Assessment. The same income tax rates and Class 4 NIC that apply to a sole trader apply to an LLP member on their profit share.

Key advantage: No employer NIC on profit distributions to LLP members (members are self-employed, not employees). At the April 2025 rate of 15%, this is a meaningful saving versus paying equivalent salaries.

LLP member with £60,000 profit share:

Income tax: £11,432 | Class 4 NIC: £2,457 | Total: £13,889

LLP Requirements

- At least two members — no maximum

- Registered office address in the UK

- Formal LLP agreement (strongly recommended — without it, the default terms under the LLP Act 2000 apply, which may not reflect your intentions)

- Annual accounts at Companies House (similar to LTD)

- Partnership Self Assessment return (SA800) plus individual Self Assessment per member

Critical constraint: If one member leaves and you fall to a single member, you have 6 months to admit a new member — otherwise it reverts to a general partnership (unlimited liability). This practical risk is why many two-person firms choose LTD instead.

| Criterion | LLP Advantage | LTD Advantage |

|---|---|---|

| Employer NIC on profit | ✅ None on profit shares | 15% on salary component |

| High earner (£100K+ per member) | 40% income tax on all profit | ✅ 19–25% CT on retained profits |

| Retaining profits to reinvest | All profits taxed immediately | ✅ Retained profits grow at 19–25% CT |

| Business sale / investment | Complex — no shares to transfer | ✅ Shares easily transferred; BADR may apply |

| Moderate profit per member (<£100K) | ✅ Often more efficient overall | CT + dividend still competitive |

✅ Choose LLP When:

- Multiple genuine partners sharing management responsibility

- Professional services sector (solicitors, accountants, architects, GPs)

- Profit per member is moderate (<£100,000) — CT + dividend route not compelling

- Professional body requires partnership structure

- You value self-employed tax status (no employer NIC on profit distributions)

❌ LLP Less Appropriate When:

- Only two partners and one might leave (reverts to general partnership)

- You want to retain and reinvest profits at a lower tax rate

- Planning to sell the business — LTD shares are simpler to transfer

- Want to bring in external investors

- Profit per member exceeds £100,000 (CT + dividend route often wins)

NIC Comparison — The Often-Overlooked Cost Driver

| NIC Type | Sole Trader | LTD Director (salary + dividends) |

|---|---|---|

| On salary/drawings | Class 4: 6% on £12,571–£50,270; 2% above | Class 1: 8% on £12,571–£50,270 (salary only) |

| Employer NIC | None | 15% on salary above £5,000 secondary threshold |

| On dividends | N/A | None — dividends carry zero NIC |

| Employment Allowance | Not available | Not available for single-director companies (available up to £10,500/yr if you have other employees) |

Tax Comparison Summary — All Three Structures

| Structure | £40,000 Profit | £70,000 Profit | £100,000 Profit |

|---|---|---|---|

| Sole Trader | Tax: £8,724 Keep: £31,276 |

Tax: ~£18,850 Keep: ~£51,150 |

Tax: ~£34,050 Keep: ~£65,950 |

| LLP (per member) | Tax: £8,724 Keep: £31,276 |

Tax: ~£18,850 Keep: ~£51,150 |

Tax: ~£34,050 Keep: ~£65,950 |

| Limited Company | Tax: ~£9,200 Keep: ~£30,800 ST marginally ahead |

Tax: ~£17,500 Keep: ~£52,500 LTD ~£1,350 ahead |

Tax: ~£26,000 Keep: ~£74,000 LTD ~£8,000 ahead |

The Decision Framework: 5 Steps to Your Right Structure

Step 1 — Do You Need Liability Protection?

If your business could create debt or legal claims against you personally — construction, professional advice, healthcare, product manufacturing, property, financial advice — limit your liability. Choose LTD or LLP. If your business has no meaningful liability risk (tutoring, copywriting, most one-person consulting where you deliver services, not products or regulated advice), liability may not be the primary driver.

Step 2 — Are There Two or More Equal Partners?

If yes and you are in professional services → consider LLP alongside LTD. If yes but you want to retain profits or plan to sell → LTD is usually better. If no → decision is between sole trader and LTD.

Step 3 — What Are Your Current and Expected Annual Profits?

| Annual Profit | Typical Recommendation | Reasoning |

| Under £20,000 | Sole trader | Tax saving too small to justify £1,000–2,000/yr extra admin cost |

| £20,000–£35,000 | Sole trader (review at £35K) | Liability risk or client requirements may override the numbers |

| £35,000–£50,000 | Borderline — model with accountant | May break even or save slightly; liability and professional image matter here |

| Over £50,000 | LTD typically beneficial | Higher-rate income tax; Corporation Tax + dividend extraction more efficient |

| Over £100,000 | LTD strongly advantageous | Significant saving vs sole trader; pension contributions and dividend strategy amplify benefit |

Step 4 — Do Your Clients Care About Your Structure?

Some clients — particularly large corporates, public sector bodies, and regulated businesses — prefer to contract with limited companies for procurement compliance, insurance, and IR35 assessment reasons. If a significant client or contract requires a limited company, that may be the deciding factor regardless of the tax numbers at your current income level.

Step 5 — Are You Caught by IR35?

IR35 is the off-payroll working legislation that catches contractors who operate through personal service companies but are functionally employees of their clients. If you are inside IR35, the tax advantage of the LTD structure largely disappears — income is treated as employment income and taxed accordingly. See IR35 Guide 2026 for the full three-test framework. If IR35 applies to your situation, your accountant should assess your status before you incorporate.

Common Mistakes When Choosing or Changing Structure

Incorporating Too Early

Before profits justify it. The additional accountant cost (£1,000–2,000/yr more), bank charges, payroll, dividend paperwork, and annual accounts overhead outweighs a modest tax saving below £35,000–£40,000 profit.

Not Taking a Proper Salary

Directors who pay themselves only dividends miss qualifying years for State Pension and may attract HMRC questions about whether dividends are genuine distributions. Most accountants recommend a minimum salary at or above the secondary NIC threshold (£5,000) to maintain a NIC record.

Treating the Company Account as a Personal Wallet

Paying personal expenses from the company creates Director’s Loan Account deductions or benefit-in-kind issues. Common HMRC targets: personal mobile phones, personal car costs, home broadband beyond legitimate business proportion.

No Shareholders’ Agreement or LLP Agreement

In an LLP or multi-shareholder LTD, a formal agreement governs what happens if a partner leaves, dies, or wants to sell. Without one, disputes are governed by default statutory rules. Have an agreement drafted when the structure is created — retrofitting one after a dispute is expensive.

Missing the Companies House Filing Deadline

Accounts must be filed within 9 months of year-end (21 months from incorporation for first accounts). Late filing triggers automatic penalties from £150, escalating steeply. Unlike HMRC penalties, Companies House penalties are applied automatically with very limited appeal grounds.

Not Reviewing the Structure as Business Grows

The optimal extraction strategy at £50,000 profit is not the same as at £150,000. An annual review with your accountant — covering salary, dividends, pension contributions, VAT scheme, and the April 2026 dividend changes — typically pays for itself.

Next Steps — Making It Official

Staying as Sole Trader

- ☐ Register with HMRC Self Assessment (deadline: 5 October following the first tax year you start)

- ☐ Register for VAT if turnover has exceeded or will exceed £90,000

- ☐ Set up Xero Simple (from £7/month — MTD ITSA-specific plan)

- ☐ Engage accountant for Self Assessment — typically pays for itself through correctly claimed expenses

Incorporating a Limited Company

- ☐ Check company name availability at Companies House

- ☐ Decide share structure (100 ordinary shares typical; consider spouse as shareholder for dividend efficiency)

- ☐ Incorporate via 1st Formations — from £12.99, same-day, registered office included

- ☐ Open business bank account (Starling/Monzo Business/Tide — free at entry level)

- ☐ Register as employer with HMRC if paying salary

- ☐ Set up Xero Grow and invite your accountant with advisor access

Transitioning from Sole Trader to LTD

- ☐ Time to tax year end (5 April) or accounting period end — mid-year changes add complexity

- ☐ Accountant closes sole trader books + files cessation period Self Assessment

- ☐ Notify clients — the company is a new legal entity; existing contracts may need novation

- ☐ Value any assets transferred from you personally to the company — capital gains considerations apply to appreciated assets

- ☐ Update all business stationery, invoices, and website with company details including registered number and registered office

Frequently Asked Questions

Q: At what income should I incorporate?

The commonly cited range is £35,000–£50,000 net profit (after business expenses). Below £35,000, additional accountant cost and administration typically consume the tax saving. Above £50,000, the saving on higher-rate income tax versus Corporation Tax + dividend extraction becomes meaningful. The April 2026 dividend tax increase narrows the margin slightly — model the specific numbers with your accountant before deciding.

Q: Do I need a registered office address?

Every limited company and LLP must have a registered office address in the UK — it appears on the public Companies House register and receives statutory mail. Many owner-directors use their home address, which is legal but makes it permanently public. 1st Formations provides a central London EC professional registered office from £39/year, keeping your home address private. See: UK Registered Office Address Services 2026.

Q: What is the difference between director and shareholder?

A director manages the company. A shareholder owns it. In a one-person company, you are typically both. In partnerships, a spouse or business partner can be a shareholder without being a director — receiving dividends without management responsibilities. Share structure needs careful design from day one; changing it later can trigger stamp duty and CGT implications.

Q: What happens to my sole trader debts when I incorporate?

Personal debts incurred as a sole trader remain your personal liability — they do not transfer to the new limited company. Going forward, the limited company incurs its own debts which are the company’s liability, not yours personally (unless you have given personal guarantees). This forward-looking liability protection is one of the key reasons to incorporate.

Q: Can I be both director and employee of my limited company?

Yes. A company director is an officer of the company and can also be employed under a contract of service. Most small company owner-directors treat themselves as employees for payroll purposes — paying a salary via PAYE and taking dividends on top. This is the standard structure and is entirely legal and recognised by HMRC.

Q: Do I need a business bank account for my limited company?

Yes, in practice. A limited company is a separate legal entity and its finances must be separate from personal finances. Mixing funds creates accounting chaos, tax complications, and HMRC scrutiny. Starling Business, Monzo Business, and Tide open accounts quickly (typically same week) with no monthly fee at entry level. See: Best Business Bank Account UK 2026.

Summary: Quick Decision Guide

Stay Sole Trader if:

- Profit consistently below £35,000

- No meaningful personal liability risk

- No clients requiring limited company

- Minimum admin is the priority

Consider LLP if:

- Two or more genuine partners in professional services

- Want liability protection + self-employed tax treatment

- Profit per partner under £100,000

- Professional body requires partnership

Incorporate LTD if:

- Profit consistently exceeds £40,000–£50,000

- Personal liability risk from your work

- Large clients prefer limited company

- Want to retain and reinvest profits

- Plan to sell the business or bring investors

- IR35 does not apply to your situation

ThriveOnz 360 — Structure + Accounting Tools

1st Formations + Xero — Incorporate and Set Up Accounting in One Day

ThriveOnz 360 Growth members: LTD vs Sole Trader Tax Calculator 2026/27 + UK Business Structure Comparison Guide (£30K–£150K profit levels) + Limited Company Setup Checklist (38 steps) + Xero 30-day free trial. Free to join.

Related Articles

UK Formation and Structure Hub

- 1st Formations vs Rapid Formations 2026: Best UK Company Formation Service — formation agent comparison

- UK Registered Office Address Services 2026: What You Need, What to Avoid — from £39/year with 1st Formations

- Best Business Bank Account UK 2026: Starling vs Monzo vs Tide vs Barclays

UK Tax and Compliance

- Making Tax Digital for Small Business 2026: Complete Guide — MTD obligations for your chosen structure

- IR35 Guide 2026: Everything UK Contractors and Hirers Need to Know — if IR35 applies, the LTD tax advantage largely disappears

- UK Auto-Enrolment Pension Guide 2026 — pension obligations once you start employing

- UK PAYE Guide 2026: How to Set Up and Run Payroll for Small Business

Accounting Software

- Best Accounting Software UK 2026: Top 10 for SMEs

- How to Set Up Xero for UK SMEs: Step-by-Step Guide 2026

- Xero vs QuickBooks UK 2026: Best Accounting Software Comparison

Last updated: February 2026. Tax figures reflect 2025/26 rates confirmed by HMRC. Dividend tax changes (basic rate 10.75%, higher rate 35.75%) take effect 6 April 2026 as confirmed by the Autumn 2025 Budget. Employer NIC rate 15% and secondary threshold £5,000 took effect 6 April 2025. Corporation Tax rates (19% small profits rate up to £50,000; 25% main rate over £250,000) confirmed unchanged for financial year beginning 1 April 2026. Class 4 NIC: 6% on profits £12,570–£50,270; 2% above. VAT registration threshold: £90,000 (from April 2024). 1st Formations pricing: from £12.99 for formation; verify current pricing at 1stformations.com. All tax calculations are illustrative estimates based on simplified assumptions — actual tax position varies based on expenses, pension contributions, additional income, and individual circumstances. This article provides general information only and does not constitute tax, legal, or financial advice. Always consult a qualified accountant or tax adviser before changing your business structure.